In case you didn't know I like Uber. Actually, no, I love Uber. I love Uber as a customer and I love Uber as an analyst, for many reasons. It's a disruptive company which has brought about huge innovation in an industry that has been largely unchanged since its inception in the early 1600s. Any company that has the ability to almost single handedly disrupt a worldwide industry as big as the taxi industry is certainly one to take notice of and investors have. The company is valued at over $60 Billion, the highest valuation ever for a private company. In it's 7 year existence Uber has surpassed the likes of Honda, Ford and Nissan, and is quickly catching up to BMW and Volkswagen. This is something that can't be ignored.

This massive valuation doesn't come from nothing though. Uber has something, it has the business model. I always believe innovative and successful companies need two things; the business model and the technology. So far I think Uber has the business model, and that's by far the most difficult bit to get right. Think how many times you've heard people say the 'Uber for X' when talking about new ideas and start-ups. 'Uberisation' has become a commonly used term, it even has it's own Wikipedia page: https://en.wikipedia.org/wiki/Uberisation

As I write this Apple has announced a $1 Billion investment in Didi - Uber's main rival in China. This is a massive technology company investing in a business model and customer base.

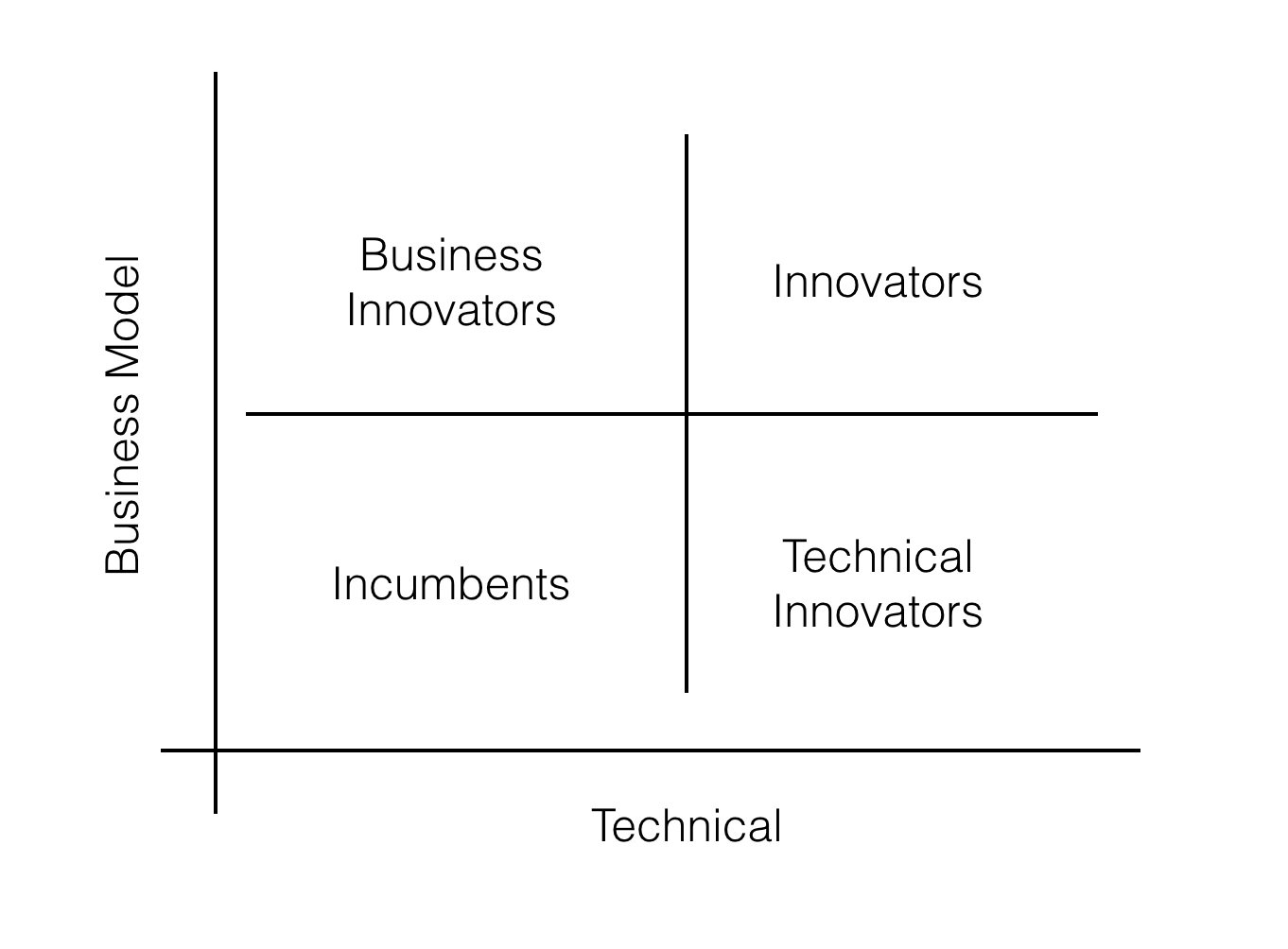

In the quad above it's easier to move right along the x-axis than it is to move upwards along the y-axis. Right now I see Uber being in the 'Business Innovators' sector.

So if Uber has got this huge valuation without the technology imagine how it will develop once it has it. But what is the technology? Well it's autonomous cars of course.

All Uber has to do now is sit and wait until fully autonomous cars become available in the next 10 years. Once this happens Uber can eliminate one of it's biggest costs, the drivers, and the service then becomes available to a much wider audience as it can charge much less. It could become as cheap as public transport for many journeys. Right now a journey from Vauxhall to Waterloo would cost £2.40 on the London Underground, and it would cost £5 on Uber Pool. Imagine how much that cost would drop if there was no driver and the vehicle was electric (It's not just about paying a drivers wages as with autonomous vehicles you potentially get much higher asset utilisation).

Now, almost every vehicle manufacturer (and some tech companies) is working on autonomous vehicles but so many of them are forgetting about the business model that comes with it. Remember that personal car ownership will die away as autonomous vehicles are introduced (Link) so how are they going to make their money? Uberisation.

You see once Uber has the technology it already has the worldwide customer base to take advantage of it while others may have the technology but have no one to sell it to.

It's true that some incumbents understand this. We've seen General Motors invest heavily in and partner with Lyft while BMW have their Drive Now on-demand service. The question is though; is this enough? And when comparing these to Uber they don't even come close.